{kind=link}

In most parts of the world, Bitcoin mining is a legal activity, but the regulations surrounding it are often nuanced and evolving. This article aims to clarify the legal status of crypto mining in various countries, offering insights into where it’s permitted and the specific rules that apply.

Let’s explore the diverse legal frameworks that impact crypto mining globally.

What Is Bitcoin?

Bitcoin is a revolutionary technology that provides a new way of transferring money. It is a decentralized currency with no physical form, and unlike traditional currencies, it is not controlled by any bank or central authority. The Bitcoin network consists of individual users who are connected to process and verify transactions, making Bitcoin secure and trustworthy.

Transactions within the Bitcoin network require no middleman; instead, users interact directly with each other to conduct secure transactions at a fraction of the cost of normal banking fees.

Overall, Bitcoin is changing how people access and transfer money around the world, granting users more control over their finances than ever before.

How Does Bitcoin Mining Work?

Bitcoin mining is an innovative method of generating new Bitcoins by using computing power to solve complex cryptographic hash puzzles.

This proof-of-work verification process, also known as “mining,” requires miners to compete with each other to find the next block in a long chain of bitcoins, and when they do, they are rewarded with newly generated coins. It’s like a race against time — miners have to be the first to solve the mathematical puzzle and add the next block to the Bitcoin blockchain. If they do it, they gain rewards in the form of newly “mined” coins. This proof-of-work mechanism keeps track of who owns what coins and enables all users to trust that their transactions will remain secure.

A Bitcoin Transaction’s Components

Three things happen when a transaction is conducted on the Bitcoin network:

- Transactional input

- Transaction output

- The sum of the transaction

A hard-to-decode cryptographic hash problem is created for each transaction submitted by the Bitcoin mining program. Then, it gathers the number of transactions necessary to create a block into the Merkle tree.

The Merkle Tree and the SHA-256 Algorithm

The Merkle Tree and SHA-256 algorithm are two of the most sophisticated technologies implemented in blockchain networks.

The Merkle Tree was invented to store data in a secure and efficient manner, while the SHA-256 algorithm is used to create cryptographic hashes that help verify the immutability of blockchain records. With these two components working together, blockchain networks become virtually impenetrable, making it impossible for malicious actors to change or tamper with transaction data without being noticed by other nodes in the network. These two technologies not only ensure security but also provide an extra layer of protection for sensitive information stored within a distributed ledger.

Why Do Bitcoins Need to Be Mined?

The Bitcoin mining process is an essential part of the Bitcoin network. It maintains stability and protects the Bitcoin ledger from malicious actors by verifying transactions on the Bitcoin blockchain.

Bitcoin miners are incentivized with mining rewards when they successfully complete a block of transactions, which then gets added to the Bitcoin ledger. These rewards constitute an important source of income for Bitcoin miners and ensure that they have a financial incentive to process Bitcoin transactions.

All of this makes Bitcoin mining an essential part of the overall Bitcoin system, as without it, users would not be able to securely transfer their funds or take advantage of all its features.

What Is Blockchain?

Blockchain technology lies at the core of digital currencies such as Bitcoin and Ethereum.

Blockchain technology is a revolutionary development in the world of digital data storage and security. It is a reliable, distributed ledger system that enables individuals, businesses, and even governments to securely store and transfer data without having to trust a third party or go through complex authorization processes.

This not only allows faster transactions but also increases transparency between all parties since transactions are stored in an immutable, decentralized system. Blockchain can also be used to verify all sorts of transactions, including financial ones such as cryptocurrency, payments, and contracts; operations with physical assets and intellectual property like land titles and copyright, respectively; medical records for doctors and hospitals, etc.

Apart from being efficient and secure, blockchain offers unparalleled opportunities to create innovative solutions for numerous industries, thanks to its unique structure.

Solo vs. Pool Mining

It has grown increasingly difficult for a solo miner to win a block and collect the block reward as the network has developed, and mining has become exceedingly popular and in demand. Bitcoin mining requires significant computational power and resources, making it challenging for individuals to compete without substantial investment. Today, buying a lot of hashing power is the only option for a solo miner to compete, but doing so is quite expensive.

Is Bitcoin Mining Legal?

In most cases, crypto miners simply need to be aware of laws regarding the use of electricity and data systems to stay compliant with local regulations. That said, many countries are slowly beginning to introduce regulations specific to Bitcoin and cryptocurrency mining in order to protect investors and set safety standards in this industry.

Is Bitcoin Mining Legal in the USA?

As of 2024, cryptocurrency mining is legal in the United States, but being governed by a mix of federal and state regulations, it faces potential changes in taxation.

Federal Regulations

The federal government does not currently ban cryptocurrency mining. However, ongoing discussions about new tax policies could impact the industry. Notably, the Biden administration has proposed a 30% excise tax on the electricity used by cryptocurrency mining operations. This proposal aims to address environmental concerns and ensure that mining activities contribute fairly to the economy.

State Regulations

Regulations can vary significantly by state:

- New York: New York has implemented a moratorium on certain types of proof-of-work cryptocurrency mining operations that use carbon-based energy sources. This law is part of the state’s broader effort to meet its climate goals.

- Texas: Texas, known for its crypto-friendly stance, is currently debating Senate Bill 1751. This bill seeks to restrict tax incentives for Bitcoin mining and limit miners’ participation in state demand response programs to stabilize the energy grid.

- Arkansas: Arkansas has passed Senate Bills 78 and 79, which regulate noise levels and energy consumption of crypto mining operations. These bills address community concerns about the environmental and local impact of mining activities.

Tax Implications

The Internal Revenue Service (IRS) treats mined cryptocurrencies as taxable income at the time of receipt. This means that miners must report the fair market value of the coins as income when they are mined. Additionally, any subsequent sale or trade of the mined cryptocurrency is subject to capital gains tax, creating a dual tax obligation for miners.

So, while crypto mining remains legal in the U.S., it is essential for those involved in the industry to stay informed about evolving regulations, tax implications, and proposed taxes to ensure compliance and optimize their operations.

Is Cryptocurrency Mining Legal in India?

As of 2024, the legality of cryptocurrency mining in India remains somewhat ambiguous. While there are no explicit laws banning or legalizing cryptocurrency mining, several regulatory developments have influenced this activity. In 2018, the Reserve Bank of India (RBI) banned banks from providing services to cryptocurrency-related businesses, which indirectly impacted mining operations. However, the Supreme Court lifted this ban in 2020, allowing for the resumption of cryptocurrency trading and, by extension, mining.

Despite this, the Indian government has considered various bills that could affect the future of cryptocurrency mining. The proposed Cryptocurrency and Regulation of Official Digital Currency Bill bans private cryptocurrencies and could make mining illegal if enacted. Additionally, mining in India faces practical challenges such as high electricity costs, lack of modern equipment due to import restrictions on ASIC mining rigs, and a 30% tax on gains from mining.

Thus, while cryptocurrency mining is not explicitly illegal in India, it operates in a gray area with tangible regulatory and practical hurdles.

Is Bitcoin Mining Legal in Canada?

Similarly to the USA, Bitcoin mining is legal in Canada, but regulations vary significantly by province. Although the federal government has not imposed a nationwide ban on cryptocurrency mining, certain provinces have taken steps to regulate the industry due to concerns about electricity consumption and environmental impact.

Provinces like British Columbia, Manitoba, Quebec, and Newfoundland and Labrador have implemented moratoriums on new mining operations since 2022. These moratoriums are primarily driven by concerns over peak electricity usage and the environmental footprint of mining activities. For instance, Quebec had initially welcomed Bitcoin mining as an economic opportunity but later imposed restrictions to manage energy consumption and environmental impact.

In contrast, Alberta has taken a more favorable stance towards Bitcoin mining. The province actively encourages investment in the digital asset mining industry, recognizing the potential benefits such as job creation, economic diversification, and international market access. Alberta’s approach has made it an attractive destination for Bitcoin miners seeking a supportive regulatory environment.

Despite the regulatory challenges in some provinces, the Bitcoin mining industry in Canada remains resilient. Companies have adapted by expanding their operations into new markets and diversifying their revenue streams. For example, Canadian mining firms like Hut 8 and Bitfarms have sought opportunities outside of Canada, in such countries as Argentina and Paraguay, to continue their growth.

Is Bitcoin Mining Legal in Australia?

Yes, it is legal to mine Bitcoin and other cryptocurrencies in Australia, and doing so should not pose many difficulties. Cloud mining, application-specific integrated circuit (ASIC) mining, and graphics processing unit (GPU) mining are all acceptable across the majority of Australian territory.

Keep in mind that cryptocurrency is not regarded as legal tender in Australia. Therefore, no business is required to accept it as a payment method, and no federal or provincial insurance is available on cryptocurrency funds.

Is Bitcoin Mining Legal in New Zealand?

Yes, Bitcoin mining, as well as mining of other cryptos, is legal in New Zealand.

However, you must pay income tax on any profits you make from mining Bitcoin or other cryptocurrencies. That’s because the Inland Revenue Department (IRD) views cryptocurrency mining as a money-making procedure.

The good news is that you can deduct most of the expenses you incur when mining Bitcoin or another cryptocurrency from your taxes. This includes expenses for hardware, electricity, and the internet.

Is Bitcoin Mining Legal in the UK (United Kingdom)?

Yes, there are no restrictions on Bitcoin mining in the UK, and the same goes for other cryptocurrencies. There is no formal regulatory system that would cover the operations of virtual currency miners.

Customs taxes are levied on imported mining equipment. Furthermore, all mined cryptocurrencies are subject to income tax and social security.

The UK’s Financial Conduct Authority (FCA) classifies cryptocurrencies like Bitcoin as “exchange tokens,” which means they are not regulated as traditional financial instruments. This classification impacts how these tokens are taxed and what regulations apply to their use and exchange. For example, businesses involved in crypto activities, including mining, must comply with anti-money laundering (AML) and know-your-customer (KYC) regulations.

List of Countries Where Bitcoin (BTC) Mining Is Illegal

Currently, Bitcoin mining is legal in the United States and the majority of other countries. However, you may want to research local laws where you live.

It is quite simple to list the countries where cryptocurrencies are completely prohibited. According to the U.S. Library of Congress, nine countries have officially outlawed cryptocurrencies. This list includes:

- Algeria

- Bangladesh

- China

- Egypt

- Iraq

- Morocco

- Nepal

- Qatar

- Tunisia

It’s also worth mentioning that, due to energy issues, Sweden advocates for an EU-wide ban on energy-intensive cryptocurrency mining methods, such as Bitcoin’s proof of work.

The increase in mining energy consumption in Sweden takes its toll on the country’s climate goals as it redirects renewable energy away from critical services. Regulators argue that the social benefits of cryptocurrencies don’t justify their environmental impact, advocating for less energy-intensive alternatives.

The crypto world is constantly changing, and what’s true today may no longer be so tomorrow. Stay updated with Changelly — subscribe to our weekly newsletter!

Become the smartest crypto enthusiast in the room

Get the top 50 crypto definitions you need to know in the industry for free

What are the Risks of Bitcoin Mining?

While the process of mining has many benefits, it also comes with some risks, and legality is not the only issue.

For starters, mining requires huge amounts of electricity, which can be an issue for power companies or countries with limited resources. Additionally, if miners aren’t careful when securing their hardware, it could be hijacked by malicious actors who could use it to mine for their own gain. There’s also the matter of market value; if the price of Bitcoin crashes prior to the validation of mined coins, miners can end up losing substantial investments from expensive hardware purchases.

Is Bitcoin Mining Profitable?

The profitability of Bitcoin mining depends on a few key factors, most notably the cost of electricity, the type of Bitcoin mining hardware, and current mining difficulty levels. While mining is often seen as a lucrative venture that can lead to significant financial gains, miners must be aware of its inherent risks and costs.

Bitcoin can also be bought on a cryptocurrency exchange if you don’t want to mine it. Due to its high price, most people won’t be able to buy a whole Bitcoin, but you can buy fractions of it on the exchanges using fiat money like dollars. If you want to buy Bitcoin with credit card (or another payment method) at a bargain price, give Changelly a chance — we’ve gathered all the best rates and lowest fees in one place just for you!

How Much Do Miners Earn From Bitcoin Mining?

The block reward and transaction fees incentivize the allocation of computing resources to the network and the continuous energy consumption required for transaction validation. A miner receives Bitcoin as payment for each block they successfully mine.

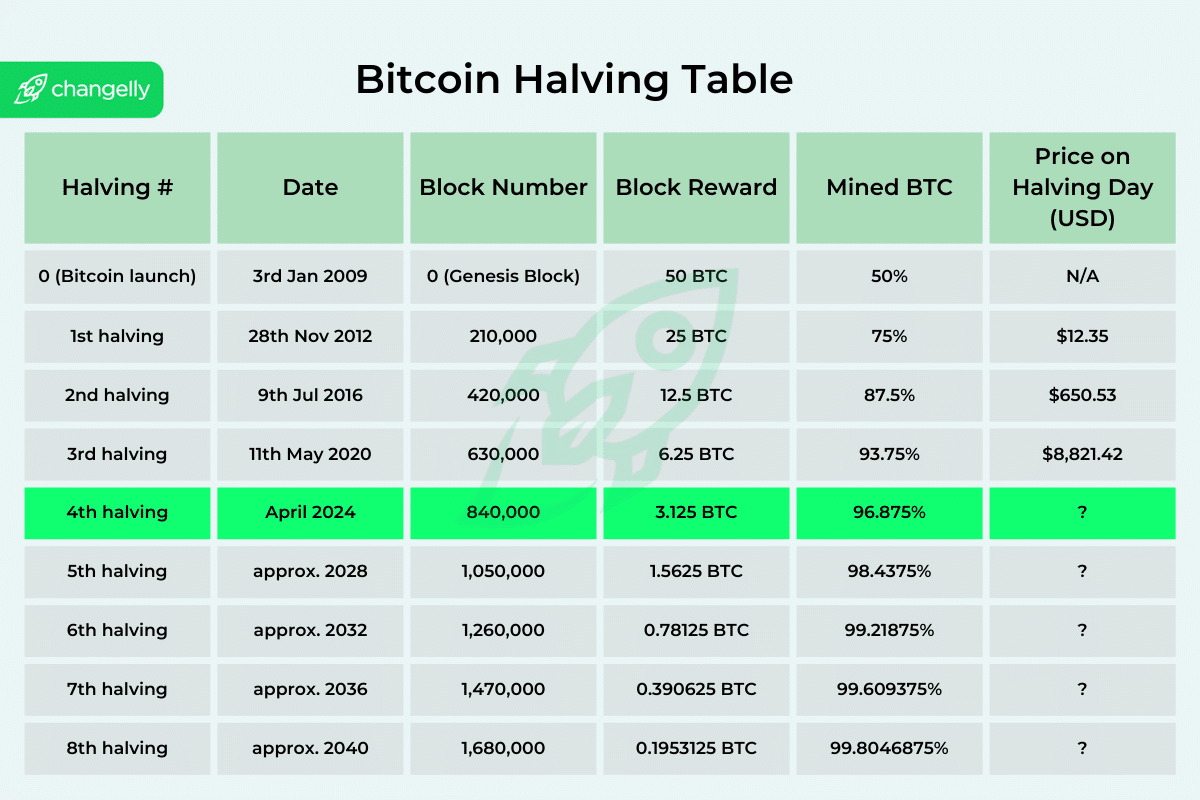

Bitcoin Halving

The block reward was initially 50 BTC for each block; however, it is now reduced by half every four years. This mechanism will be applied until block rewards exist no more. Today, the block reward is only 3.125 BTC after being cut in half four times.

Why Does Mining Use So Much Electricity?

Crypto mining is becoming more and more relevant as digital currencies dominate the financial landscape, but why does it require so much electrical power?

The answer lies in blockchain technology, which is the digital backbone of cryptocurrency that allows information to be shared and transactions to be verified. A cluster of computer processors is needed to solve complex mathematical equations and record digital transactions in the blockchain network, making them unchangeable and secure. This means that as digital currencies such as Bitcoin become more popular and hence have more transactions conducted via their chains, additional electricity is consumed.

Therefore, the future of cryptocurrency mining may require more renewable energy solutions with fewer emissions if it is to be sustainable over time.Furthermore, some experts warn that as more and more people join the mining process, solving increasingly complex algorithms will require even more powerful machines. This may lead to a massive energy drain that could have detrimental implications for global carbon emissions.

FAQ

Still have a question? Don’t worry, Changelly got you covered! Here’re the answers to burning questions.

How long can it take to mine 1 Bitcoin?

Instead of mining one Bitcoin, crypto miners create one block, with the payout set at 3.125 BTC for each block. It takes 10 minutes to produce one Bitcoin block. This implies that theoretically, mining 1 BTC will only take 10 minutes (as part of the 3.125 Bitcoin reward).

However, it’s crucial to understand that thousands of Bitcoin miners are vying for a payout for each block.

Does Bitcoin mining give you real money?

It gives you a reward in the form of cryptocurrency: when a fresh block of Bitcoin transactions is verified, Bitcoin miners are rewarded with payments in Bitcoin. They can further exchange their crypto coins for fiat money any time they want.

Is it risky to mine Bitcoin?

Yes, mining Bitcoin can be risky. The main risks include high costs for electricity and hardware, which can make mining unprofitable if Bitcoin prices drop. Additionally, mining difficulty increases over time, requiring more advanced equipment and more power. There’s also regulatory uncertainty in many countries, where changes in laws can suddenly disturb mining operations.

How much does it cost to mine 1 Bitcoin?

The estimated cost to mine 1 Bitcoin after the 2024 halving ranges from $30,000 to $35,000. Generally based on averages, it can vary significantly depending on the country, with deciding factors including electricity prices, climate (which affects cooling costs), and the efficiency of mining hardware.

What happens if I mine 1 Bitcoin?

Then you’ll have 1 Bitcoin! Just kidding. Unfortunately, this is an almost impossible situation. Even with optimum hardware and software, which isn’t always accessible (only a select few can afford it), it takes mining pools (not solo miners) a lot of time and energy to compete over winning the race and adding a new Bitcoin block.

However, any rule has exceptions: in January 2023, the battle to add block 772,793 to the Bitcoin blockchain was won by a solo Bitcoin miner with an average hash rate of just 10 TH/s (terahashes per second).

Since the total hash rate of Bitcoin at the time the block was added was just over 269 exahashes per second, the solo miner’s hash rate of 10 TH/s only accounted for 0.000000037% of the computing power used to create the blockchain.

Simply put, it was a very unlikely victory for a solo miner, and this case actually made history.

How do BTC miners get paid?

For confirming a fresh block of Bitcoin transactions, Bitcoin miners receive incentives that are paid in BTC. Miners who successfully validate the block receive a reward of 6.25 BTC. Depending on the market price, this may be a substantial sum.

How do BTC miners get paid?

For confirming a fresh block of Bitcoin transactions, Bitcoin miners receive incentives that are paid in BTC. Miners who successfully validate the block receive a reward of 3.125 BTC. Depending on the market price, this may be a substantial sum.

Who pays Bitcoin miners?

The blockchain pays for Bitcoin mining You may think of the blockchain as a miner’s employer. As a result, the “employer” foots the bill for Bitcoin mining rewards.

Bitcoin mining does not belong to anybody or anything. Then, from where does the Bitcoin reward come?

Bitcoin users are the source of the reward. To pay the miner, the blockchain utilizes some amount of Bitcoin whenever the miner approves your transaction. The blockchain records millions of transactions daily, so there is enough Bitcoin to pay the miners.

Can you mine Bitcoin on your iPhone?

No, Bitcoin mining on the phone is not feasible, at least not in the conventional sense.

How do you join the Bitcoin mining pool?

It’s not difficult to sign up for the Bitcoin mining pool. You can join one by pointing your ASIC miner to a particular stratum address that the pool provides. We discuss BTC mining pools in detail in this article.

Is Bitcoin mining just free money?

No, Bitcoin mining is not just free money. While it can be profitable, it involves significant costs and risks.

Disclaimer: Please note that the contents of this article are not financial or investing advice. The information provided in this article is the author’s opinion only and should not be considered as offering trading or investing recommendations. We do not make any warranties about the completeness, reliability and accuracy of this information. The cryptocurrency market suffers from high volatility and occasional arbitrary movements. Any investor, trader, or regular crypto users should research multiple viewpoints and be familiar with all local regulations before committing to an investment.